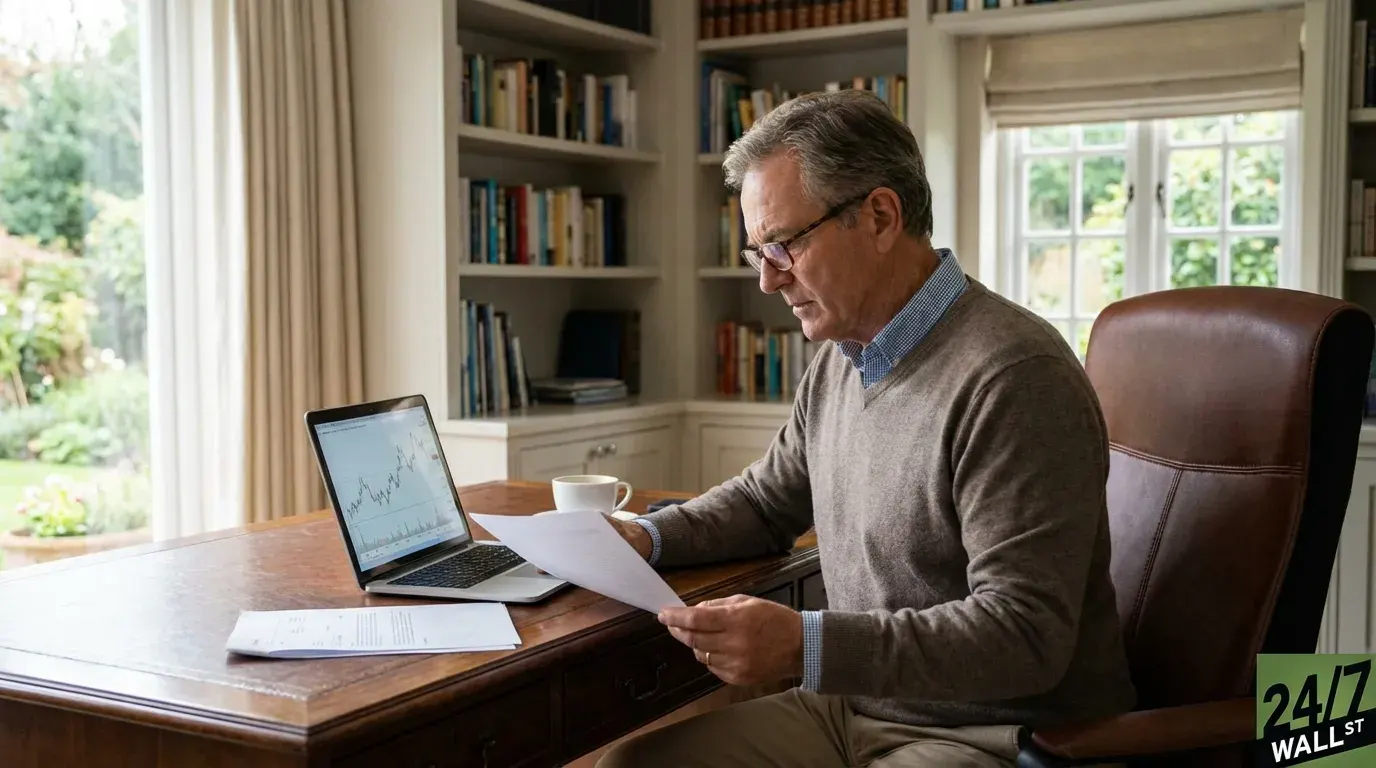

"After decades of work and disciplined saving, he entered retirement with a simple rule: "I cannot afford to lose money." So he shifted to a 30% stocks, 70% bonds allocation. That feels safe. But in practice, playing defense this aggressively reduces his sustainable income by about $340 a month right now, and the gap widens with time."

"The central tension is not volatility versus safety. It is purchasing power survival versus the illusion of safety. A 30/70 portfolio has historically returned approximately 5.5 to 6% annually, while a 60/40 portfolio has returned approximately 7.5 to 8%. That difference sounds modest until you run the numbers over a 20 or 30-year retirement."

"At a 4% withdrawal rate, both portfolios generate $76,000 per year at the start, the divergence appears in what is left behind. The conservative 30/70 portfolio grows at roughly 1.5 to 2% after withdrawals, while the balanced 60/40 portfolio grows at 3.5 to 4% after withdrawals. That compounding gap is where real damage accumulates."

"After 10 years: the 30/70 portfolio shrinks to approximately $1.65 million, while the 60/40 portfolio grows to approximately $2.05 million. The sustainable monthly withdrawal from each reflects that divergence: $4,100 per month from the conservative portfolio versus $4,440 per month from the balanced one. That $340 monthly gap compounds."

A 65-year-old retiree with $1.9 million saved uses a rule of avoiding losses by holding 30% stocks and 70% bonds. This allocation feels safe but lowers sustainable income by about $340 per month and widens the gap over time. The issue is purchasing power survival rather than volatility alone. A 30/70 portfolio has historically returned about 5.5% to 6% annually, while a 60/40 portfolio has returned about 7.5% to 8%. With a 4% withdrawal rate, both start near $76,000 per year, but the conservative portfolio grows only about 1.5% to 2% after withdrawals versus 3.5% to 4% for the balanced portfolio. After 10 years, the conservative portfolio is about $1.65 million versus about $2.05 million for the balanced portfolio, producing lower monthly withdrawals.

#retirement-planning #asset-allocation #withdrawal-strategy #stock-vs-bond-risk #portfolio-sustainability

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]