#do-insurance

#do-insurance

[ follow ]

#homeowners-insurance #insurance #real-estate #california #auto-insurance #extreme-weather #insurance-costs

#homeowners-insurance

SF real estate

fromNonprofit Quarterly | Civic News. Empowering Nonprofits. Advancing Justice.

8 hours agoIs your state becoming uninsurable? We have the latest data. | Nonprofit Quarterly | Civic News. Empowering Nonprofits. Advancing Justice.

The U.S. faces a homeowner's insurance crisis due to rising costs and extreme weather impacts.

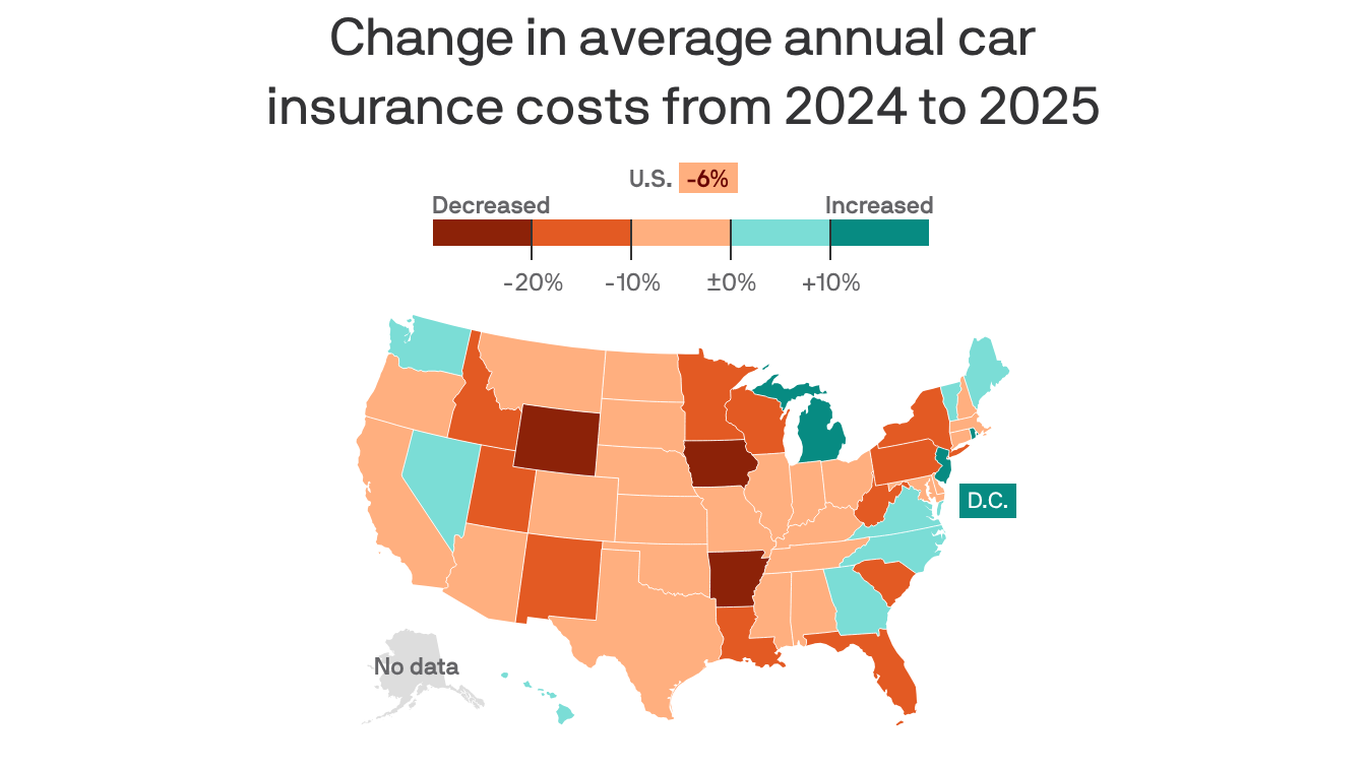

#auto-insurance

NYC parents

fromwww.amny.com

1 month agoOp- Ed | Hochul's proposed auto insurance reforms would be a death sentence' for traffic violence victims | amNewYork

Proposed changes to auto insurance laws in New York may harm victims of traffic accidents by limiting their recovery options and redefining serious injuries.

fromAol

2 months ago7 Insurance Moves That Won't Leave You High and Dry, According to Brokers

Insurance is often one of those bills people think about only when premiums rise or a loss makes it necessary to review. Not updating a policy can cost you vastly more money than just paying a slightly higher premium, be that car insurance, home insurance or life insurance, to name a few. Rather than waiting to find out what coverage you have, brokers and other insurance experts offered some moves you should make as soon as possible.

Health

fromwww.theguardian.com

2 months agoHow extreme weather is leaving thousands of homes uninsurable

We're seeing more frequent, more severe extreme weather events and that inevitably affects claims and affects pricing it can't not. And this is happening all over the globe. More, after this week's most important reads.

Environment

Real estate

fromwww.housingwire.com

1 month agoHow Builders Strengthen Mitigation & Insurability in a Hard Market

Insurance carriers now require mitigation features as baseline standards rather than optional upgrades, with demonstrated risk reduction directly correlating to lower premiums and improved insurability.

fromFortune

1 month ago$15 billion of the insurance industry is at risk from AI, BofA says | Fortune

Our view is that large-language model digital agents can effectively do a non-immaterial portion of the work currently provided by 20-30k independent agents across the United States. The core of the firm's bearish thesis centers on a massive pool of routine, low-complexity insurance policies.

Artificial intelligence

fromStreetsblog

1 month agoThursday Headlines: Insurance Who Insurance Why Edition - Streetsblog Empire State

Part of the issue is the black box that is insurance. The state Department of Financial Services helps set rates for companies operating in New York, but on a granular level, companies use proprietary algorithms and metrics to set premiums.

US politics

fromHigh Country News

2 months agoAs the planet heats, insurance premiums rise - High Country News

Last November, two Washington residents filed a lawsuit accusing petroleum corporations of misleading the public for decades about fossil fuels' effect on climate change and how global warming is harming the planet and its inhabitants. Their lawsuit marks the latest addition to the growing number targeting Big Oil. The case, however, was novel, given the plaintiffs' damage claims: That increased carbon emissions from fossil fuel burning have intensified extreme weather events, such as hurricanes, wildfires, floods and heat waves.

Environment

fromLos Angeles Times

1 month agoState Farm reaches deal to keep 17% hike in home insurance rates

The agreement will provide financial relief to many policyholders while ensuring continued coverage for State Farm policyholders while California's insurance market stabilizes. State Farm argued the emergency hike was necessary because catastrophic fire losses jeopardized its financial ratings. The company has reported that it paid out $6.2 billion in claims last year, largely from the wildfires, with most of the costs covered through reinsurance payments.

LA real estate

fromEntrepreneur

2 months agoHow to Keep Your Health Plan Costs Manageable - Without Shortchanging Your Team

If you run a business, there's a familiar email you probably opened this fall: the one from your benefits broker with your 2026 health insurance renewal. You scroll. You see a double-digit increase, and your stomach drops. You want to do right by your team. You also have a P&L to protect. And the three standard options you're handed - pay the increase, raise deductibles or push more cost onto employees - all feel bad in different ways.

Business

US politics

fromStreetsblog

2 months agoGov. Hochul Is Playing With Toys - And The Facts - In Latest 'Propaganda' Video on Car Insurance: Lawyers - Streetsblog New York City

Gov. Hochul's proposal would bar crash victims from recovering damages if found 51% or more at fault, prompting trial lawyers to condemn it as insurer-friendly.

from24/7 Wall St.

1 month agoWhy the First 5 Years of Retirement Are the Most Dangerous for Your Portfolio

A market downtown in the first few years of retirement, combined with regular withdrawals, can permanently damage a portfolio's ability to sustain income over time. The same downturn occurring 10 or 15 years later, when withdrawals have already been funded by earlier growth, does far less harm.

Retirement

Real estate

fromRedfin | Real Estate Tips for Home Buying, Selling & More

2 months agoHow to Protect Your Client During Underwriting

Underwriting verifies buyer finances and property eligibility, requiring thorough documentation and proactive communication to prevent income, documentation, or property issues from delaying closing.

Real estate

fromwww.housingwire.com

2 months agoRealtor associations add health insurance benefits for members

ORRA and ABoR offer members subscription-based, unlimited access to comprehensive national healthcare teams, reducing unpredictable costs for independent real estate agents and supporting wellbeing.

[ Load more ]