"That's a $9,000 raise, essentially. Sell the car and use that cash to get a functional car. If you can sell it, get that $5,000 in your hand plus this $9,000 and buy you a $15,000 paid-for car, that's a nice car. And now you got no car payments."

"The $740 monthly car payment is the single most important number in her budget. That car payment alone consumes $740 every month going toward a depreciating asset she may owe more on than it is worth. Eliminating it does not just free up cash flow. It removes a fixed obligation that compounds her vulnerability every month she stays in debt."

"Opportunity cost is what you give up by choosing one use of money over another. Every dollar going toward a $740 car payment is a dollar that cannot attack a credit card likely charging well above 20% annual interest."

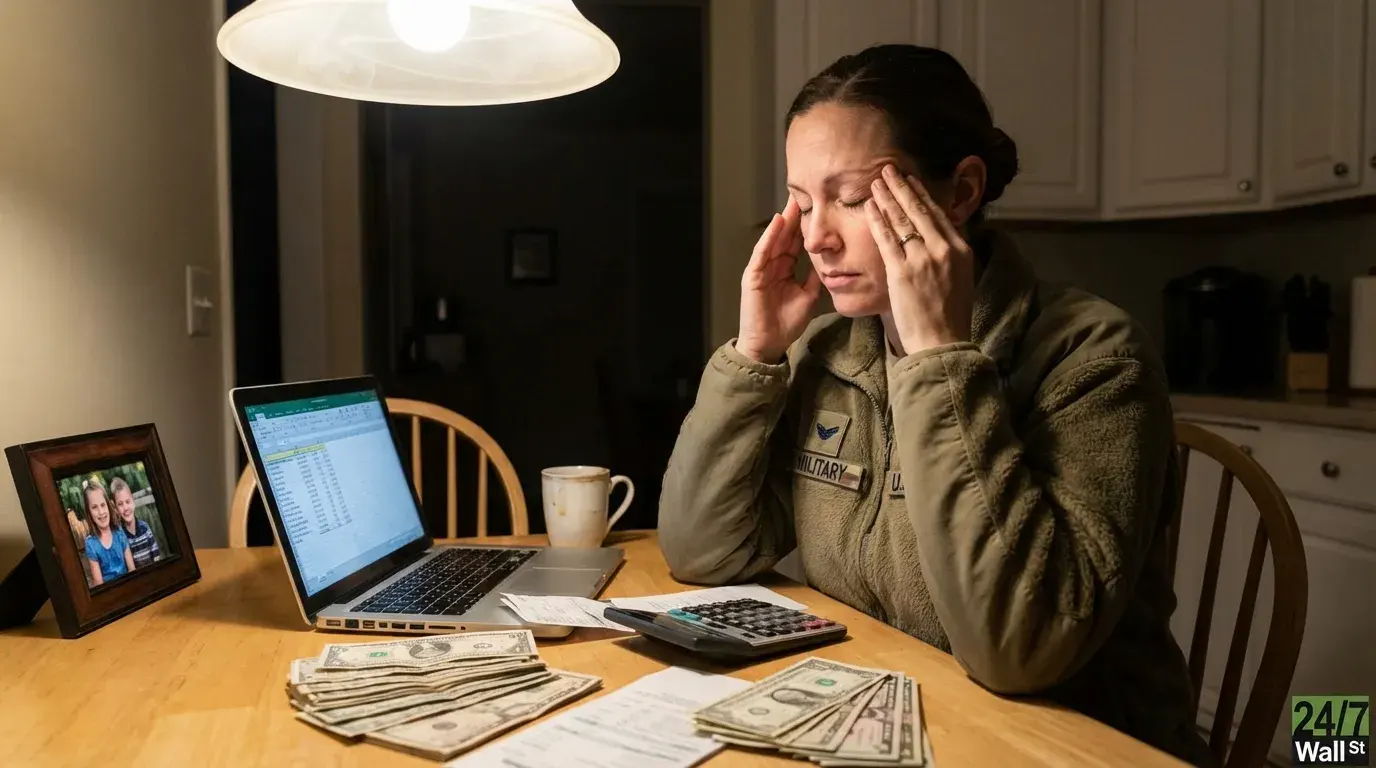

A 40-year-old single mother working three jobs earns $102,000 yearly but carries $112,000 in debt across a $30,000 car loan, $24,000 personal loan, $30,000 deferred student loans, and multiple credit cards. Her $740 monthly car payment represents the largest drain on her stretched budget. Financial advisors recommend selling the vehicle and using her $9,000 in savings plus the sale proceeds to purchase a $15,000 paid-for car, eliminating the monthly obligation. This strategy frees up $740 monthly cash flow to attack high-interest credit card debt. The core principle involves opportunity cost—every dollar spent on a depreciating asset is a dollar unavailable to combat debt charging over 20% annual interest.

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]