#mbs-treasury-spread

#mbs-treasury-spread

[ follow ]

#inflation #federal-reserve #interest-rates #treasury-yields #monetary-policy #us-dollar #dividend-stocks

fromLondon Business News | Londonlovesbusiness.com

5 days agoUS dollar stable near recent highs - London Business News | Londonlovesbusiness.com

Escalating geopolitical risk continued to dominate global markets' concerns, with safe-haven demand keeping the dollar index anchored near a multi-week high.

World politics

#us-dollar

US Elections

fromLondon Business News | Londonlovesbusiness.com

3 days agoUS dollar rose amid a rebound in geopolitical concerns - London Business News | Londonlovesbusiness.com

The US dollar strengthened due to geopolitical fears and better-than-expected economic data, while uncertainty keeps market volatility high.

US Elections

fromLondon Business News | Londonlovesbusiness.com

3 days agoUS dollar rose amid a rebound in geopolitical concerns - London Business News | Londonlovesbusiness.com

The US dollar strengthened due to geopolitical fears and better-than-expected economic data, while uncertainty keeps market volatility high.

fromFortune

6 days agoBond yields are falling even as oil tops $102, showing that Wall Street fears recession more than inflation | Fortune

"Oil prices are higher again this morning, but Treasury yields are lower as the risks to economic growth begin to take precedence over the risks to inflation," Oxford Economics said in a note on Monday.

World news

Retirement

fromLondon Business News | Londonlovesbusiness.com

2 days agoEvery time you borrow from a bank, you're paying more than you think - London Business News | Londonlovesbusiness.com

Opportunity cost in loans includes lost potential earnings from repayment dollars, not just the interest rate paid.

World politics

fromLondon Business News | Londonlovesbusiness.com

6 days agoUS dollar stable after successive gains - London Business News | Londonlovesbusiness.com

Escalating Middle East tensions are influencing market sentiment, keeping the dollar stable and impacting US Treasury yields amid inflation concerns.

from24/7 Wall St.

2 days agoHow Income Investors Are Using HYBL to Dodge Interest Rate Risk in 2026

HYBL attempts to solve the income problem by combining senior loans, high-yield corporate bonds, and debt tranches from U.S. collateralized loan obligations (CLOs). The result is a portfolio with lower duration and lower volatility compared to traditional high-yield funds, while still targeting high current income with monthly distributions.

Business

from24/7 Wall St.

3 weeks agoGoldman Sachs Engineered a QYLD Competitor Yielding Over 10%

QYLD has been running the covered call playbook on the Nasdaq-100 since December 2013, and with $8.3 billion in assets, it remains the dominant fund in this category. The strategy is straightforward: hold the Nasdaq-100 and sell covered call options against the entire index each month, collecting premium that gets distributed to shareholders as income.

E-Commerce

Venture

from24/7 Wall St.

3 weeks agoYieldMax's Buffett Tracking BRKC Pays 2.78% While Treasuries Yield 4.15%, and That Gap Is Hard to Ignore

BRKC uses synthetic covered calls to generate monthly distributions from Berkshire Hathaway exposure, but caps upside potential while offering 2.78% yield below the 4.15% Treasury rate, with underperformance versus BRK-B since launch.

from24/7 Wall St.

2 days agoThis ETF Pays Dividends Monthly and Yields 7.3%

The fund blends high yield corporate bonds, senior loans, and debt tranches of U.S. collateralized loan obligations (CLOs) into a single actively managed portfolio, aiming to deliver income that beats the broad bond market while keeping volatility lower than any single segment on its own.

Business

US politics

from24/7 Wall St.

3 weeks agoStagflation Fears Are Returning: Grab These 5 Safe High-Yield Dividend Kings Now

Stagflation risks are rising due to weak job growth, persistent inflation, and structural economic changes, requiring investors to consider defensive dividend stocks that historically perform well during such periods.

fromFortune

2 weeks ago300 years of wars show they are 'always disaster times' for holders of government debt because of inflation and financial repression | Fortune

"The historical evidence reveals a striking pattern: government bonds have repeatedly generated substantial real losses during these extreme episodes. They have even underperformed equities and real estates which are traditionally regarded as risky assets."

World politics

UK news

fromLondon Business News | Londonlovesbusiness.com

2 weeks agoUK rates: Savers, investors should act now in higher-for-longer era - London Business News | Londonlovesbusiness.com

UK interest rates will likely remain elevated longer than expected due to renewed inflation threats from energy prices and geopolitical tensions, requiring savers and investors to adjust their financial strategies accordingly.

from24/7 Wall St.

3 days agoUSHY Yields 6.58% While VIX Sits at the 96.5th Percentile, A Risky Tradeoff

USHY seeks to track the investment results of the ICE BofA US High Yield Constrained Index, composed of U.S. dollar-denominated, high yield corporate bonds, providing broad exposure in a low-cost wrapper.

Business

UK news

fromLondon Business News | Londonlovesbusiness.com

2 weeks agoBank of England holds base rate amid Middle East war - London Business News | Londonlovesbusiness.com

The Bank of England held the base interest rate at 3.75% due to Middle East conflict uncertainty and rising energy prices threatening inflation expectations.

Miscellaneous

from24/7 Wall St.

1 month ago3 Clear Winners When Exploring High-Yield Savings Accounts

High yield savings accounts and money market funds offer FDIC-insured returns of 3.3% or higher with full liquidity and no early withdrawal penalties, making them attractive alternatives to traditional CDs in volatile markets.

from24/7 Wall St.

3 days agoJPMorgan's Short-Duration JPIE Earned 15.24% Since Inception While the Bond Market Cratered

JPMorgan Income ETF has delivered over 50 consecutive monthly distributions since its October 2021 inception, providing stability that is the entire point of the investment strategy.

Business

Business intelligence

from24/7 Wall St.

4 weeks agoThe 4 ETFs To Buy Before The Fed Lowers Rates And Shoots Them Higher

The Federal Reserve paused rate cuts in January 2026 after three cuts, creating market uncertainty that underprices assets benefiting from future cuts, with four ETFs positioned to capitalize on eventual rate reductions.

fromLondon Business News | Londonlovesbusiness.com

3 weeks agoDollar surges on geopolitical risks and rising yields

Crude oil breaking above the USD 100 threshold has revived inflation concerns, pushing US Treasury yields higher across the curve. However, Friday's labour market report revealed a significant deterioration in employment conditions, with the economy losing 92,000 jobs in February, its largest contraction in several months.

World news

US news

fromLondon Business News | Londonlovesbusiness.com

1 month agoDollar Relatively Stable Amid Economic Uncertainty - London Business News | Londonlovesbusiness.com

The dollar remains stable within a consolidation range, with its direction dependent on monetary policy expectations, labor market data, and inflation trends.

from24/7 Wall St.

4 days agoWall Street Bullish on Americas Gold and Silver: BMO Sees Major Re-Rate Ahead

BMO believes Americas Gold has the expertise to execute its optimization strategy, particularly at the Galena Complex, and sees the company's approach increasing free cash flow generation as production grows organically.

Business

Real estate

fromwww.housingwire.com

1 month agoThe 200-Basis-point gap: Why many lenders are leaving money on the table

A persistent 200 basis point performance gap between top and bottom tier lenders reflects structural industry inefficiency, not cyclical conditions, with top lenders earning 139 basis points while bottom lenders lose 70 basis points.

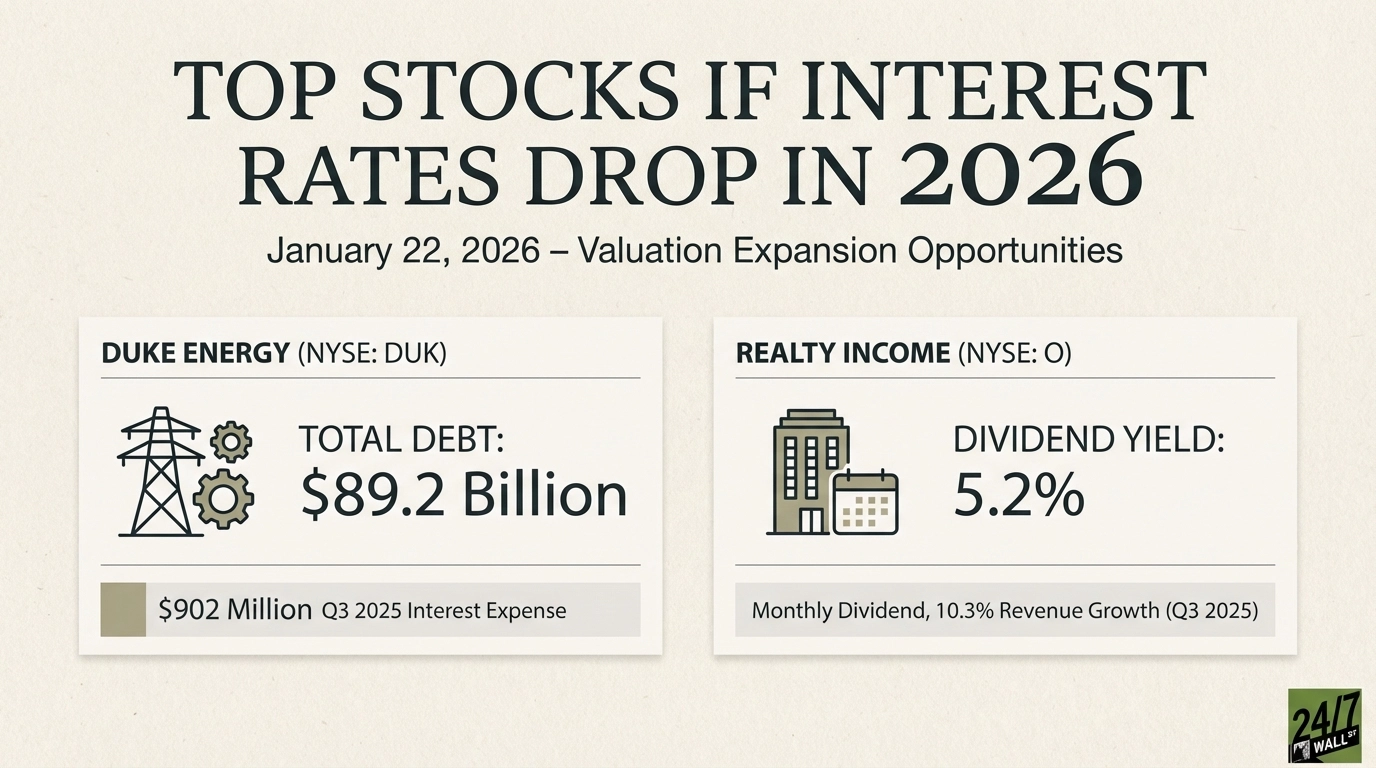

from24/7 Wall St.

4 weeks agoInterest Rates Are Heading Down - These 3 Stocks Win Big When They Do

In my view, interest rates are more likely than not going to head lower over the course of 2026 and into 2027. I'm not saying we're due for a pandemic-like selloff, but I do think that weakness in the labor market is likely more protracted than the government data suggest. As such, I do think the makeup of the Federal Reserve, and which way many of its presidents and voting members lean (toward providing support for the labor market over battling inflation) could lead to much faster rate cuts than many think.

Retirement

Education

fromLondon Business News | Londonlovesbusiness.com

1 month agoThe right way to learn investing: Practice before theory, systems before tactics - London Business News | Londonlovesbusiness.com

Practice investing through real decision-making before deep theory to build systems and muscle memory that perform under market stress.

Business

fromSilicon Canals

1 week agoGold crossed $5,300 the same week three central banks quietly dumped $47B in US Treasuries. That's not coincidence - it's coordination - Silicon Canals

Gold's price surge is driven by strategic positioning of central banks, not just fear, as they reduce US Treasury holdings amid geopolitical tensions.

from24/7 Wall St.

1 month ago3 ETFs to Buy ASAP Before Jerome Powell's Term Ends in May

Warsh served on the Fed's Board of Governors from 2006 to 2011, making him the youngest person ever appointed to that role at age 35. During the 2008 financial crisis, he was part of Ben Bernanke's inner circle and served as an intermediary with Wall Street. He negotiated survival plans for firms like Morgan Stanley (NYSE:MS). He later resigned from the Fed due to disagreements over its balance sheet expansion policies.

US politics

Business

fromLondon Business News | Londonlovesbusiness.com

2 weeks agoUS dollar stable after Fed decision and stronger yields - London Business News | Londonlovesbusiness.com

The dollar strengthens near 100 as the Fed maintains a cautious stance, while Treasury yields rise on reduced rate cut expectations amid higher inflation projections and Middle East tensions driving oil prices up.

Business

fromLondon Business News | Londonlovesbusiness.com

2 weeks agoWhere is the US Dollar Index heading amid rising bond yields? - London Business News | Londonlovesbusiness.com

The US Dollar Index strengthens due to Federal Reserve's hawkish stance, elevated Treasury yields, and geopolitical tensions, with limited rate cuts expected through 2027.

fromLondon Business News | Londonlovesbusiness.com

2 weeks agoSilver under Fed pressure and geopolitical support - London Business News | Londonlovesbusiness.com

The current decline in silver prices is not merely a temporary correction, but a deeper repricing of market expectations regarding the path of U.S. interest rates, which remains the most influential factor in the short term for non-yielding assets.

Business

Business

fromFortune

2 weeks agoU.S. debt is competing with a record supply of corporate bonds, which is pushing up the cost of federal borrowing just as war spending piles up | Fortune

Record corporate bond issuance driven by AI capital expenditure and geopolitical factors is increasing Treasury yields and raising borrowing costs for the federal government.

Business

fromFortune

2 weeks agoA 'debt spiral,' before a fiscal crisis: interest on the national debt will be growing faster than GDP in just 5 years, think tank warns | Fortune

By 2031, U.S. federal debt interest rates will exceed economic growth rates, triggering a self-reinforcing debt spiral where deficits cause debt to grow indefinitely.

from24/7 Wall St.

1 month agoRate Cuts Are Eating Into BIZD's Income and Total Returns Are Suffering

BDCs function like closed-end lenders: they raise capital, lend it to private companies at floating interest rates, and are legally required to distribute at least 90% of taxable income to maintain their tax-advantaged status. This structure makes BDC income highly predictable in its sourcing, if not its magnitude.

Business

fromFortune

2 months agoBonds 101: What investors need to know about the 'shock absorber of the portfolio' | Fortune

Many investors regard bonds as the frumpier cousins to stocks. Their prices rarely pop or plummet. They usually deliver a lower return, and-aside from a glamorous cameo in the 1980s thriller Die Hard-they are not part of popular culture in the same way as, say, GameStop or Tesla shares. They are, though, a critical part of any well-managed portfolio, and with the stock market looking particularly frothy, this may be more true than ever.

Business

fromLondon Business News | Londonlovesbusiness.com

2 months agoDollar struggle and monetary policy shape the next phase - London Business News | Londonlovesbusiness.com

The resilience of gold above $4,800 per ounce at this stage reflects a delicate and complex balance between traditional supporting factors and emerging pressures-one that cannot be superficially interpreted or reduced to the movement of the dollar alone. It is true that the U.S. dollar's retreat from its recent peaks, after failing to sustain its recovery momentum from a four-year low, provided gold with a short-term breather and attracted some buyers.

Business

from24/7 Wall St.

2 months agoWhat I'm Watching Before Buying JP Morgan's Active Bond ETF

The JPMorgan Active Bond ETF (NYSEARCA:JBND) charges a premium for active management, but has attracted $5.4 billion since its October 2023 launch by delivering outperformance when markets get volatile. The real test ahead is whether managers can continue generating alpha as corporate bond spreads compress to levels not seen in two decades. The Spread Squeeze That Could Define 2026 Corporate bond spreads have compressed to their tightest levels in two decades, creating a challenging environment for active managers.

Business

[ Load more ]